WTF Are Stablecoins?

A primer on how stablecoins work and what they promise for the economy

If this is your first time reading Uncredentialed, welcome! This is a community of 88 people committed to learning, thinking, and doing, instead of resting on their credentials. If that sounds like you, help make the community grow to 89 strong!

👋Hi friends,

I hope you all had a good holiday week! Personally, I’m excited to be getting back into my regular rhythm here on Uncredentialed. This week we’ll be diving into understanding stablecoins and what they might offer. Let’s jump in!

WTF are Stablecoins?

Evolution of Money

Efficiency has a certain gravity to it. One place this is abundantly clear is the evolution of money and banking.

Barter and Trade

Thousands of years ago, as the agricultural revolution pushed humans to transition from a nomadic lifestyle to living in villages, towns, and cities, we still lived in a pre-money world. Everything was settled by barter and trade. You need some sheep’s wool but don’t have any sheep? You’ll have to negotiate with your neighbor to compensate him with an appropriate number of your chickens.

This, of course, was highly inefficient. Lots of time wasted negotiating and renegotiating every time you need something, not to mention the chain of trades needed if the person with the sheep’s wool wants something you don’t have (i.e., having to trade with someone to trade with someone to eventually trade with the person who has what you want).

Commodity Money

Eventually, this migrated into a form of what we call “commodity money”. It became clear that certain resources were in high demand, regardless of your specific need for them. Things like sheep, cattle, and salt were universally desired so, when trading, I might be willing to accept someone’s salt even if I have no current need for it, knowing I’ll be able to pawn it off to someone else who does need it.

This helped reduce the number of negotiations required to facilitate a trade, but trade was still done on an ad-hoc, negotiated basis, and you had to be holding a sizable, often perishable, resource in the interim.

The Metal Era

Once people grew accustomed to accepting commodities that they themselves didn’t plan to use during trades, it wasn’t too large a leap to transition to using metals as a medium of exchange.

In the 7th century BC, the kingdom of Lydia (modern day Turkey) pioneered the metal era by releasing “electrum” coins, stamped with a seal certifying the weight and value of the asset1. Standardized mediums of exchange supercharged trade, streamlining the negotiation process and paving the way for the first era of global trade as the Silk Road rose to prominence.

Paper Money

By the 7th century AD, the standardized medium of exchange that coins provided was an unquestionable success, but lugging around so much metal became a burden, so China invented the promissory note. Merchants could deposit their metal with proto-deposit banks in exchange for pieces of paper bestowing the rights to those coins. Merchants could then exchange these papers freely without needing to actually have any coins with them.

These grew in popularity, with the first state-sponsored promissory notes being released around 1023 AD and a full transition to paper money happening by the 13th century AD. The idea slowly expanded west, eventually becoming the standard in Europe during the 18th century AD.

Fiat Money

While paper money removed its holders a step further from any connection to tangible, real-world value, it still held ties to a physical asset. But not for long. Following World War 1, attempts to align domestic holdings of gold with paper currency were non-trivial factors in the Great Depression and the rise of nationalism that led to World War 22.

After World War 2, the nations came together to create the Bretton Woods system, where the US Dollar (USD) would be pegged to gold, and all other currencies were pegged to USD. This entered most currencies into a quasi-fiat system, where their currencies didn’t tie directly to any tangible asset (though they weren’t truly fiat, because they still indirectly tied to gold via USD).

This lasted until 1971 when President Nixon officially untethered the US Dollar from gold, transitioning the global monetary system to a truly free-floating fiat system.

Plastic Money

Concurrent with the transition to fiat money came the emergence of charge cards and the leading card networks, Visa and Mastercard. Just like paper money before it allowed people to stop carrying so many coins with them, cards allowed people to stop bringing paper money with them. People could simply go about their shopping with their card and later on, would true up the amounts they owed with their bank, paying back with paper money.

Digital Money

Lastly came the computer wave. As computers became ubiquitous, our monetary system was not left behind. The rise of online banking, along with peer-to-peer platforms like PayPal and Venmo meant you could go your entire life without touching paper money. Click a couple buttons on a computer and money will leave your savings and pay off your credit card.

In the past decade, this has gone even a step further with the rise of Apply Pay and Google Pay. Future generations may not even need touch cards, let alone cash, when making purchases out in the world.

In a short few thousand years we’ve gone from a world where you have to barter every transaction using resources you’ve cultivated yourself to a world where you can make all the purchases you need while bringing nothing you wouldn’t already choose to carry (your phone) with you.

While the monetary system we live in today is many many many orders of magnitude more efficient than it was, there still are inefficiencies in the system begging to be fixed. Processing fees on transactions charged by card networks act as a friction cost on spending and, while your bank account records a transaction nearly instantly, it takes multiple days for banks to settle transactions on the back end.

Stablecoins may mark the next phase in the evolution of our monetary system, reducing processing fees and settlement delays.

So… What are Stablecoins?

At the highest level, stablecoins are a cryptocurrency pegged to a real-world asset. Theoretically you could have “GoldCoin” tied to real-world gold and leave the fiat system, but for all intents and purposes, these tend to be tied to cash or cash equivalents.

Now, if you’re anything like me, “cryptocurrency” and “scam” are indelibly joined at the hip, so you might be a little hesitant to think stablecoins have the potential to be anything more legit.

In fact, as I prepped for this post, I’ve heard comments such as, “Oh, I didn’t know you were into Bitcoin” and “Please don’t tell me you’re becoming a CrytpoBro,” so it seems safe to say the stigma is real.

Stablecoins should have no connection to the meme above. It’s in the name, they’re meant to be stable. A stablecoin tied to USD should always equal $1. In practice, there’s 3 approaches stablecoin issuers use to maintain price stability: fiat-backing (the good), algorithm-backing (the bad), and crypto-backing (the ugly).

Fiat-Backed (The Good)

Fiat-backed stablecoins are emerging as the winner in the space. They are by far the most trustworthy and reliable because their stability is maintained by 100% liability coverage. For every $1 coin issued, they hold $1 of USD or short-term US treasuries. With the passing of the GENIUS act in 2025, these issuers are audited monthly to ensure 1:1 reserves are being maintained. The most famous of these, and the one I’ll probably mention in later examples, is USDC, issued by Circle.

Algorithm-Backed (The Bad)

Unlike fiat-backed stablecoins, algorithm-backed ones are not backed by any actual asset. Instead, they try to algorithmically predict the supply and demand of their stablecoin, minting and destroying coins from the supply according to those predictions, in an attempt to keep the price stable. While a neat idea (maybe?), these add an unnecessary extra layer of risk which makes their widespread adoption into our financial infrastructure unlikely. Back in 2022, one of the largest players in the space, UST, collapsed, leading to a loss of $40B. I just don’t see a future for these.

Crypto-Backed (The Ugly)

Lastly are crypto-backed stablecoins. These maintain stable prices despite being backed with a risky asset through what’s called overcollateralization. One example is DAI. For every $1 coin of DAI that users mint, they deposit $1.50 of Ethereum to maintain a margin of error on the reserves and account for price volatility. While it’s good that they’re accounting for the fact it’s backed with a risk-on asset, I still don’t see a world where these have widespread adoption, both because of the riskiness of the backing and the inefficiency of overcollateralization.

What will Stablecoins Change?

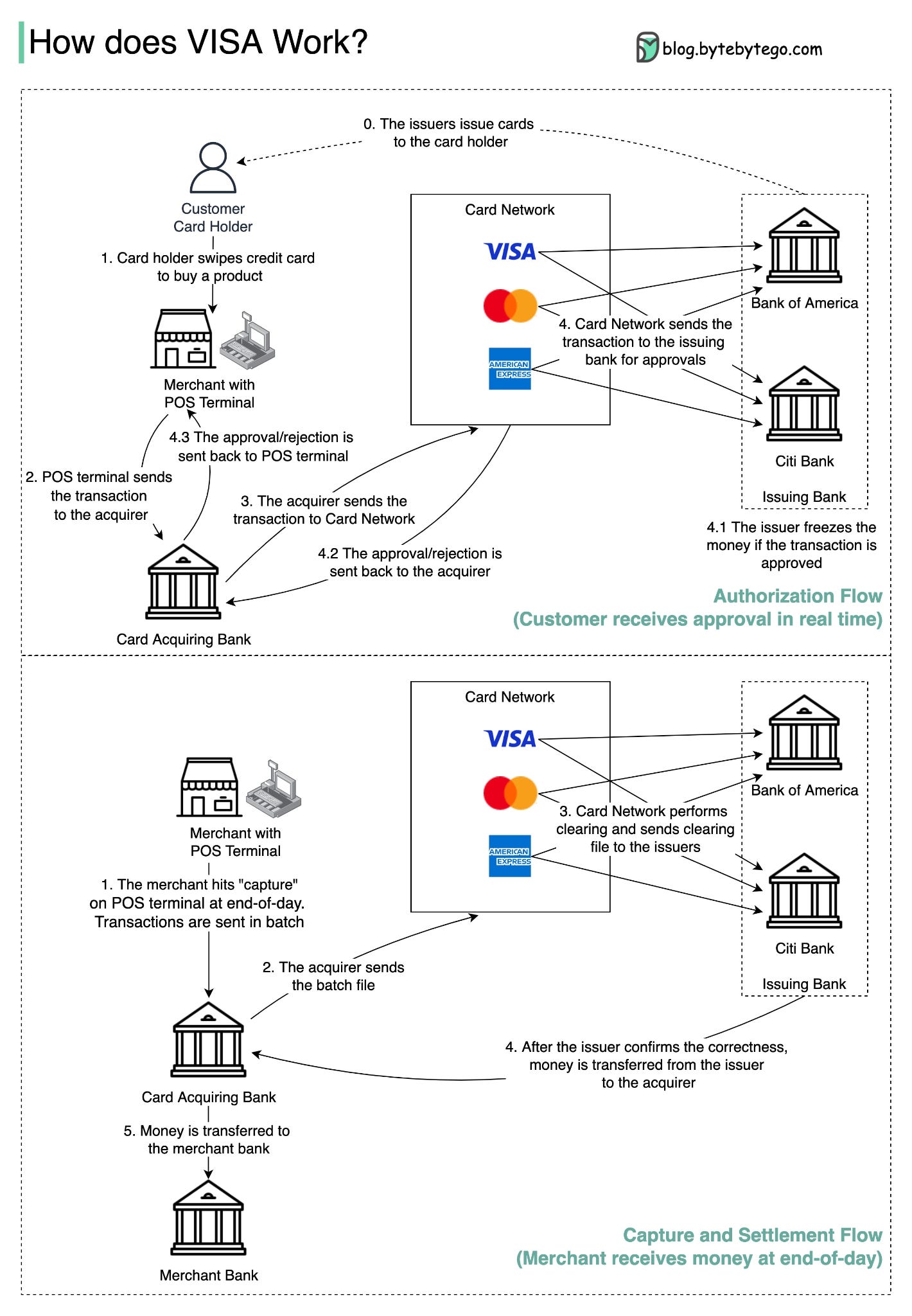

To see the impact that transitioning to stablecoins could bring, we first have to look at how transactions today work.

Modern Transaction Flow

Let’s say you’re buying $100 worth of groceries at the store. The first step in the process will be swiping your card (or using Apple Pay, but let’s ignore that for simplicity’s sake) in the Point-of-Sale (POS) Terminal. The POS Terminal will then send to what’s called the acquirer bank, which is responsible for handling that store’s transactions. The acquirer then sends the transaction information to the card networks (like Visa or Mastercard) who pass it along to the “issuing bank,” which is the term used for the bank associated with your card, AKA your bank.

Your bank then approves/declines the purchase and, if approved, will freeze the funds needed for the transaction in your account. They’ll then send word of approval back up the notification stream all the way to the POS Terminal via the card networks and acquirer bank.

The POS Terminal goes on to approve the transaction and everyone goes about their days.

Then… nothing for a bit.

Finally, at the end of the day, the merchant will capture all of the transactions from the day in its POS Terminal and send a batched version of them out to the acquirer bank. This bank passes the info along to the payment networks who distribute it to the proper issuing banks in a process called “clearing”. The banks verify these statements for correctness, find the net flow of capital between the various banks for the day, and transfer the necessary amount to the acquirer bank. Last but not least, the money is sent from the acquirer bank to the merchant’s bank, often hitting their accounts 1-3 days after the transaction occurred.

Online transactions are fairly similar, the key difference is that the POS Terminal is typically replaced by a payment processor like Stripe or Adyen, but for today’s purposes we can think of them as more or less the same.

Stablecoin Transactions Today

The transaction flow for stablecoins is much simpler. Assuming you already have USDC in your wallet, let’s say you’re buying $100 worth of books from an online retailer that accepts USDC. When you click to checkout, your stablecoin wallet would create a transaction on a public ledger, writing 100 USDC to the stablecoin wallet of the merchant, signed by your private key (this is an oversimplification, but think password) to prove authenticity.

The blockchain network would then verify that the transaction signature is correct and you actually have 100 USDC in your wallet and, assuming all is well, the merchant will be the proud owner of your 100 USDC in the blink of an eye.

Transaction fees are tiny (there are some fees for the compute used to process the transaction, called gas fees, but these are getting exponentially smaller) and the merchant receives funds nearly instantly. There’s still a number of issues, though. This would require everyone from your grandparents to Home Depot creating crypto wallets and holding USDC, something I just don’t see happening at scale. Also, unlike transactions today, these would be irreversible, even in cases of fraud.

Instead, I think the promise of stablecoins is as an upgrade to our financial infrastructure, used behind the scenes by banks to reduce frictions and delays in the transaction process.

Future Stablecoin Transactions

In my opinion, the future of stablecoins is not in being held by consumers, but by being the asset traded back and forth between banks following transactions. When you go to checkout, the transaction information would be processed by a payment processor like Stripe (who also has fraud detection and other important security items built in upfront) who would then post the transaction to the public ledger at which point the money changes hands.

To minimize gas fees, there would still likely be a degree of batching involved, maybe aggregate transactions by the minute or the hour, but much more frequently than the once-a-day aggregation that goes on today.

It sounds like a boring, minute detail, but by reducing transaction fees and settlement timings, not to mention foreign exchange headaches, stablecoins could act like a gas pedal on the global economy. They could be particularly exciting in the B2B and startup space, where transactions are larger, international transactions are frequent, and cash conversion cycles are top of mind, allowing them to accelerate reinvestment of earnings, juicing economic growth.

What Comes Next?

This all sounds great and progress is accelerating, but we’re not there yet. In the past year, the GENIUS Act laid out a regulatory framework for stablecoins, a consortium of 10 prominent banks shared plans to work on stablecoins pegged to G7 currencies, and Stripe continued to add to its portfolio of stablecoin-powered products.

For thousands of years, our monetary system has evolved towards efficiency. Betting against that continued growth is betting against our financial history. The evolution may take years or decades, but the efficiency that stablecoins promise seems inevitable.

Note, for this post’s purpose I focused on the implications to our financial infrastructure, ignoring the other promise that stablecoins provide – programmability.

Theoretically, companies could issue their own stablecoin tied to specific rules as a way of transferring money. So, for example, if Substack wanted to create an advertisement feature that allowed creators to earn money for ads, they could launch their own stablecoin that automatically transfers from advertisers to creators based on the views the post earns.

I’ve downplayed the programmability angle just because of my core thesis that stablecoins can’t hit scale until they get beyond the crypto-focused UI. Basically, I believe those use cases will come about (and some prominent companies endorsing them early could even help bring about the ecosystem-level change!), but before programmable stablecoins become a ubiquitous part of our economy, I think they need to build trust with the public through the endorsement of our financial institutions.

If you enjoyed this post, consider sharing with a friend! And if you haven’t already, subscribe to Uncredentialed to receive weekly takes on tech, startups, and strategy!

Electrum is an alloy of gold and silver

If the connection between money and central banking to global events in the 20th century is of interest to you, I highly recommend checking out Lords of Finance. I also enjoyed reading Keynes' essay, Economic Consequences of the Peace.